What you need to know about store finance credit cards

If your fridge has just broken and you don't have money to pay for a new one, a store finance credit card could help you make that emergency purchase. But before signing up, you should know a credit card's terms and conditions, fees and charges back to front. This way you can be confident you'll make monthly repayments on time, and save your future self both a huge debt and a huge headache.

What is a store finance credit card?

Store finance refers to an alternative payment option that lets a customer take home a major purchase, but defer payment to later dates. For example, if you need a new laptop but don’t have enough money saved to buy one outright, you can request store finance.

This requires you to sign up to a credit card first (usually in-store, but some retailers accept online purchases). Interest-free financing is more likely to be offered by superstores and other major retailers. For example, Harvey Norman, JB Hi Fi and The Good Guys will offer you the Latitude Finance GO Mastercard or Gem Visa card if you pass their credit checks.

What can you buy using a store finance credit card?

An eligible purchase, which means the item qualifies for a promotional interest-free offer made by a participating retailer.

Big-ticket items like furniture, whitegoods, flooring and solar panels, among others. You can even help finance a holiday, as Flight Centre and Luxury Escapes are retail partners of some cards.

Emergency purchases that are essential. Most store finance cards have a minimum credit limit of around $1000, and high purchase rates make using them for everyday purchases needlessly expensive. If you want to make a smaller purchase but can’t pay upfront, many stores offer Afterpay as their store finance option, instead of a credit card.

How does a store finance credit card work?

After being approved for the card, you’ll be put on an interest-free payment plan, also called a 0% interest payment plan. Payment plans range from 6, 12, 18, 24 or 60 months, as well as variants like 500 or 1000 days. For this duration, you are exempt from paying any interest on your purchase. There are a few different types of repayment options, outlined below. Often the promotional offer will dictate how you make repayments.

Buy now, pay later

This is often marketed by retailers as the most flexible way to pay. For the duration of the interest-free period, you’re not required to pay any deposit, interest or repayments.

However, this can be very risky business as you can get to the end of the interest-free period having paid back $0. You’ll then be hit with whopping interest rates that will make the total cost of the plan much higher than if you’d bought the item outright.

Instalment plans

These come in two forms: a minimum monthly repayment plan (with the option to pay back higher amounts) or equal monthly instalments, which split the cost of the product into even repayments. For example, a $2,000 purchase on a 6 month plan would be split evenly into around $333 per month.

A word of caution about store finance credit cards

While not worrying about paying interest on your purchase right now sounds pretty great, be mindful that the interest-free period is going to end at some point. If you haven't paid off your purchase when this happens, you’ll be stung with a high interest rate – for example 25.90% p.a. for the GO Mastercard.

When you add on other fees like those listed below, you could be revolving around debt for years on end. Make sure you read the Key Fact Sheet and Product Disclosure Statement for your interest-free credit card, to be aware of the following rates and charges.

- Establishment fee: Also called the application fee, this is the one-off fee charged for setting up your account.

- Account servicing fee: Also labelled a monthly account keeping fee, this is sometimes charged if you have a balance owing that’s higher than a specified amount, e.g. for the GO Mastercard it’s $10.

- Annual fee: Even if your card doesn’t specify an annual fee, calculate the cost of the monthly fee x 12 months for the equivalent sum.

- Purchase rate: This is the interest rate you’ll be charged when you use your store finance credit card to make everyday purchases. While you can use it to pay for groceries, petrol and dining out, etc., you shouldn’t – unless you want to be hit with a purchase rate of 20% or higher. This is why it’s prudent to save your store card for emergency purchases.

- Cash advance fee: Charged when you use the credit card to receive cash, for example in an ATM withdrawal where you choose 'credit' as the account type.

- Late fees: If you one of your minimum monthly payments, you’ll cop a late fee, which is typically around $20-30 per missed payment.

- Expired promotional purchase rate: The interest rate you'll be forced to pay if you haven't paid off your purchase by the end of the interest-free period. This is called a billed finance charge and can have your debt spiralling out of control.

How do you stop a billed finance charge on your credit card?

To avoid paying a ridiculous interest rate after the promotional period ends, you should be confident you can meet your repayment obligations, each and every month. If you're not sure if you can repay on time, you should steer clear of store finance credit cards to avoid stress and a lower credit score.

Calculate the monthly repayment amount required to absolve you of any outstanding debt by the promotion’s expiry date. This amount will be higher than the minimum monthly repayment a finance provider specifies in your statement.

To find out how much you need to pay every month to avoid interest, you can go to the moneysmart.gov.au interest-free deal calculator.

While the fees below seem pretty hefty, it can get much worse when you don't pay on time. If your balance isn’t fully paid at the end of the interest-free period, your debt may become unmanageable. The longer the interest-free period you choose, the more fees and interest you will accrue.

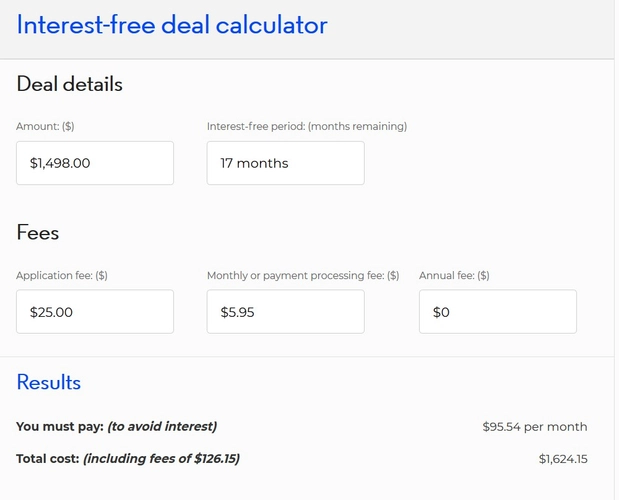

Example 1: 500 days interest free

Let’s say you wanted to buy a Asus ZenBook 14-inch i5 laptop which costs $1, 498.

You then find a 500-day interest-free promotional offer on computer products from Harvey Norman, and sign up for the GO Mastercard.

After inputting the details, you can see the minimum amount you need to repay is $95.54 per month, and you’ll be paying $126.15 in fees on top of this.

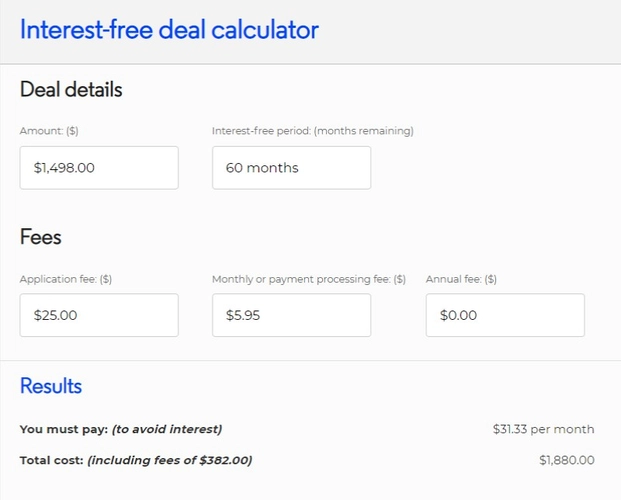

Example 2: 60 months interest free

If you're set on the Asus ZenBook but can't afford $95.54 per month, you might prefer to calculate the total over a 60-month interest free period.

As you can see, a longer interest-free period brings down the required monthly repayments to $31.33. However, you’ll be paying $382 in fees.

Now add online payment fees of 0.95 cents per month for 60 months ($57), which totals $439 in fees over 5 years.

Alternatives to a store finance credit card

There are many potential pitfalls of a finance credit card – mainly the high interest rates you’ll be hit with if you can’t pay off the debt by the promotional expiry date. As a result, consider other ways to pay first.

- Savings: Of course, the safest and most reliable way to pay for a major purchase is to budget for the expense and have a savings goal.

- NILS (No Interest Loan Schemes): These provide finance for essential household items if you’re on a low income.

- Lay-by: While the item won’t be available to take home immediately, lay-by is a more financially sound choice than a store credit card. You’ll pay off your debt in equal repayments, without any interest.

Conclusion

In summary, always approach store credit cards with caution, as they attract high fees and can pose a problem with debt if you haven't paid off a purchase by the end of the interest-free period. Only decide to apply if you've thoroughly done your research, the item you're buying is for an essential or emergency purpose, and you don't have any other ways of paying.