Best Health Insurance

To see the best health insurance plans, start by providing a few details about yourself:

RT Health Insurance 🏆 2026

4.9Award Winning, Affordable, Not-For-Profit Health Insurance.

Teachers Health Fund 🏆 2026

- See all

Excellent service, no pressure to sign anything. Sandy was very easy to chat with and very helpful. Helped me understand what my private health policy actually covers and what I actually need. Highly recommend! Show details

RT Health 🏆 2026

- See all

Dushyant Chopra was extermely knowledgeable and professional in providing me options to amend my cover. He discussed the options in great detail… Read more

answering my quiries on some complex topics with various permutations

Please compliment him on his excellent customer service

AIA Health Insurance 🏆 2026

- See all

Cody was super helpful and explained everything very clearly to ensure we understood all the important details. Show details

Queensland Country Health Fund

I was able to personally, have my refund processed expeditiously Show details

Phoenix Health Fund

We were thinking of increasing our level of extras cover which would have cost more. Phoenix gave us independent advice so that we could see what… Read more

suited us. We decided to keep the same level of cover without increasing it. We were impressed that the Phoenix rep also knew about the proposed changes to the government rebate which was very helpful.

see-u by HBF

Looking to obtain insurance for the first time. Was feeling overwhelmed with the process. Spent alot of time on the phone asking hundreds of questions - nothing was too much trouble. Lucy was fantastic to deal with Show details

Westfund Health Insurance

I am unable to access eye care or dental services, as they are exclusively located in Lithgow. It is unclear why additional centers are not… Read more

available. The staff are excellent; however, their unavailability on weekends, particularly Saturdays, is unfortunate, especially in urgent situations. While the staff application and processes are effective, updating waiting periods within the app is a complex and slow endeavor. Although a waiver was processed efficiently, any further updates require a considerable amount of time to reflect in the application. I cancelled and returned to prior fund due to delay in waiting periods on app I'm complex case but low claims. I am currently awaiting a partial premium refund, which has been pending for five days.cant change cover online or in app.also may still do cheque refunds ! For cancellation refund of premiums which I found in my account today they said would go back to bank account but went elsewhere their backend process needs work I think

Australian Unity Health Insurance

- See all

The worst you can get in Australia. My wife spent a year on it and was cursing my decision each time I had to claim anything. There is no clinic in… Read more

Australia that knows this health insurance, which means every time you have to upload your receipts online with proof to claim anything.

Allianz Care

- See all

Unprofessional people with no hour to their own commitments. Whenever I have reached them out for any reason, from all 2 years, they are experiencing… Read more

higher volumes of queries and claims than usual which eventually means it is their standard unprofessional practice.

Peoplecare Health Insurance

I’ve been with Peoplecare for over 10 years and find them fabulous to deal with. They are easy to contact and the person who answers the phone always… Read more

solves the problem and/or answers the question. Claiming is incredibly easy and payment quick and seamless. Very pleased to be a member.

Nurses & Midwives Health

- See all

Lodging a claim was quick and easy and and the advisor, Jenn, was knowledable and very helpful. Show details

TUH Health Fund

- See all

Health Insurance for Seniors is often difficult to navigate. I always phone TUH directly as their staff are knowledgeable and have time to explain. Thank you. Show details

Frank Health Insurance

Signed up for Frank as they had a promotion. Advertising a waiver on the waiting period of 2 month and 6 month extras. Submitted a claim and they… Read more

rejected it based on waiting period. Been on the phone for over 30 minutes and they’re telling me I’m wrong, even though I have a screenshot of the promotion. Stay away! I will be reporting them to the relevant consumer protection bodies

Hi Jacinta, This doesn’t sound right,… Read more

GMHBA Health Insurance

- See all

Absolute nonsense! As if I know what a clearance certificate is? Went to these guys through one of those compare services and the entire family was… Read more

put on 12 months wait. Now my wife and I can claim but not the kids. Looking to cancel now, you know what? Freedom to just do what we like when we like feels pretty fun. No more trying to wring value out of $1000/year. Bye bye!

ItsMy Health Insurance

I was very happy with the service I received. Matt was very patient and answered all my questions regarding health insurance in a lot of detail. The whole process was very easy. Many thanks! Show details

Police Health

- See all

I was in Police Health back in the 1990's but a marriage change and I was in BUPA for 20 years but now have rejoined and I'm extremely happy with their policy and service and very happy to be back. Show details

ahm Health Insurance

- See all

They are really great and able to get help when you need it. We aren’t particularly well off and they have some really affordable plans and their hospital cover has been a lifesaver. We have been with them for about 8 years now and highly recommend. Show details

HBF Health Insurance

- See all

Thier app never works, i have given up on it, I installed it because the CARD never worked.. now every time you log in to use it throws you to their… Read more

internet page on your mobile device, no point if your waiting at the counter...

so you pay the full bill you try and log in on the internet at home .. this used to work well.. but no you get the sms etc ETC wont let you in .... but it then says theirs a problem their end..

so you call them.. then push button upon button to get to the right area, then wait the mandatory 30 minutes to an hour..

all while listening to them tell you... to use the app or the internet ... which doesn't work.. also they always have audio problems as they... yell on some of their adds ...then go really quite.. on others..

if you actually wait long enough.. someone's answers, they are usually most helpful.. full points

oh if you think carrying the card works .. don't bother,

all this does is annoy the person in the shop who is try to help you.. it usually doesn't work..

to make a claim you could try using the firefox browser which seems to have worked this time.. send a photo .. then wait the mandatory 2-3 weeks. ( update guess they read the review, claim paid the next day)...

used to be so easy when you could just stand in a que and hand over the documents..

Defence Health Health Insurance

Good all-round service and support from the team at Defence Health Show details

Health Partners

We have been with Health Partners for more than 30 years and know them to be very supportive, personal and professional at all times. Many… Read more

competitors have tried to entice over the years but we have no intention of moving. Great service, products and caring people. Danny Perkins

Doctors' Health Fund

This company is a disgrace. I have been a member now for many years and I am paying nearly $10,000 a year in premiums. I rarely make claims but… Read more

recently I had a hospital admission and submitted my claims soon after. These people give me the runaround constantly. They blame Medicare, Medicare blames them and then they both blame the provider and the only person that suffers me. I’ve spent over two hours on the phone with them in the past week and each time someone has given me a different answer or reason to why my claim is being held up. They make dreadful errors at my expense and when you email them to try to find out what’s going on, they either ignore you or respond with a single line and you are no better informed than you were previously. I will be getting out of this health fund as soon as I possibly can. Please think very carefully before joining them because if you need to make a claim, they will not pay it and they will make mistake after mistake and you will be chasing your tail for months on end until you finally give up because they wear you down. I outlaid $36,900 for a procedure and so far I have received $900 back. I pay top hospital cover. That is an absolute disgrace.

HCF Health Insurance

- See all

Absolutely disgusted with customer service. I decided to switch to another fund where I'm getting the same cover for less. I got interrogated as to… Read more

why I'm switching and wanted to get down to the fine details. Lady was just plain rude. It's none of anyone's business why I'm switching, and the more you interrogate me the more I'm convinced it's the right choice. After many years of being with this health fund, I'm utterly, utterly disappointed. In a cost of living crisis, my expenses are my business - end of story. Find yourselves another health fund that values their members!

Union Health

You can tailor your health insurance to what suits you and your family. Consultants are knowledgeable and helpful. Prices are better than other providers. Show details

HIF (Health Insurance Fund)

To What if ….. I appreciate Hif as a health fund but I am over companies who don’t notify you when they are changing their systems : after failing… Read more

to be able to use my card and paying in full , I have had two 30+ minute phone calls about not being able to update my app info and having to use a downloaded claim form that I submitted only to have to call again - as I was asked what I wanted to happen next …. Only to learn that my claim Had not landed despite getting the automated response … hoping a more direct. Email provided will help … going to Physio again ( great by the way) . Tomorrow … what would happen if I did not have funds to pay?? When I have just paid a years “ enrolment “ !! ….

- review of above : great response from consumer help but still unable to get app up and running after another hour on the phone and no capacity to know when sorted but card worked at Physio - But warning: no matter what they say initially if you have to receive a code on your phone finally as can’t use your phone to register you need TWO devices for task completion. However they say they’ll send me $100 gift card but it won’t get back practice I missed and cannot make up! And I’d prefer the latter! This kind of issue is going on at Telstras new security version. . Not the fault of the person I spoke to At Hif who halve to answer the call . They were always trying to help …

Please inform call staff about time frames

Health Care Insurance

Great service and easy to use insurance – Pretty happy with HCI. Easy to use app and always been easy to get through to them over the phone. Great service and they go out of their way to help you. Show details

St. Lukes Health

This non-profit health insurer offers generous cover, but has some notable drawbacks. Their fixation on Tasmanian wellness centres is irrelevant to… Read more

mainland customers. Seems to be for Tasmanian who are not fund members. Backend systems are slow and unreliable, with occasional outages. The UX is inconsistent and feels unpolished. Expect more call centre contact than you'd get with comparable providers, and tansaction processing times of 3–5 days that feel like a throwback to the era of batch processing. The app is third-party.

The software is a grab bag of forms that are printed out, the scanned via OCR. The design is… Read more

Latrobe Health Services

We were members of La Trobe Health for over 20 years and had one of their Family Gold Top Hospital cover policies. When we attempted to review the… Read more

policy some 12-16 months ago to see whether it was still fit for purpose we were advised by La Trobe customer service that the policy we had was: * no longer available, * better than available covers and worth keeping. No mention was made of the fact that our policy would make us liable to the Medicare surcharge. We followed the advice received and kept our Gold Top Hospital Cover. This year, we received a letter from the ATO stating that we did not hold an appropriate level of private patient hospital cover and that therefore we were liable to pay $2,036 Medicare surcharge. When contacted La Trobe about this and received no satisfactory response regarding their failure to advise that the policy they suggested we keep would result in us having to pay the Medicare surcharge. This incompetence has caused us to have to pay in excess of $4,000 that we would not have had to pay had the proper advice been received from La Trobe if we had been given the information to allow us to choose the appropriate cover. We have now cancelled our policy and moved to another insurer that provided us with the comprehensive information required for us to make an informed decision. Conclusion: do not rely on the customer service received from La Trobe as you run the risk of getting incomplete, inadequate and defective advice likely to be costly. Best to move elsewhere.

Hi Juan Felipe T Thank you for your… Read more

Medibank Health Insurance

- See all

Update: After multiple follow-ups and a formal complaint, the $90 HICAPS claim has now finally been reversed. I’m glad the issue has been resolved,… Read more

although the process took several weeks and required repeated escalation.

Review Incompetent online customer service team. A false claim on my private insurance. I’ve been chasing up my refund for three weeks, but they keep procrastinating and giving me different versions of the story every time I call, completely wasting my time. They keep telling me it’s been processed, yet I still haven’t received my HICAPS refund after three weeks.

Hi Alexia. Should you feel that we have serviced your… Read more

Navy Health

I was recently diagnosed as pre-diabetic and high cholesterol and my doctor put me on a preventative drug regimen to try to address it before it… Read more

became a health issue. Navy health refused my claims even though I had not claimed any of my pharmaceutical benefit previously. Not only that they refused to respond to me personally even though both my husband and I are ex-navy and listed on the policy. Don’t bother with them you can get better service and more flexible premiums elsewhere.

Hi Sam, Thank you for your feedback. We're sorry to… Read more

NIB Health Insurance

- See all

WORST EXPERIENCE I HAVE EVER HAD WITH HEATH INSURANCE I work for an insurance company. So I know my ins and outs with health insurance better than… Read more

most. I have had multiple problems with nib since switching from Australia Unity. I signed up with nib in late may. For starters, when I signed up it took them over a month to send me my health insurance statement for the policy, as well as any welcome packages. It then took me to call them to send this through and the lady who I spoke to was absolutely rude and said it was somehow my fault that I didn’t receive it and that maybe I hadn’t checked my emails properly. It also took them almost two months to get my transfer certificate and apply it. Even when I manually sent to to them myself, as well as Australian unity sending them one. When I did finally get that sorted, I found that I had to wait another 12 months for my major dental, when I have already served the waiting periods and my annual limits were not higher than the ones I had with Australian unity. They then proceeded to tell me I had to wait another extra 6 months for my optical. Again, I had served the waiting periods for $200 and only needed to serve the 6 months for the extra $50. When I contacted them about this and questioned them. They cancelled my policy without my permission. And now I am left with no cover at all. I have even tried contacting them about this but I get no reply.

As someone who sells health insurance and one being NIB, I can absolutely say. I will NOT ever be offering anyone NIB, ever again. And I will be making it clear that NIB is not a trustworthy health fund.

We hope this message finds you well Jameson, and we're so… Read more

RT Health Insurance 🏆 2026

4.9Award Winning, Affordable, Not-For-Profit Health Insurance.

Private health insurance in Australia

When you first take out private health insurance, you will need to decide if you require one or a combination of the following options:

If you don’t want any of them, you’re still covered for public hospital visits and basic checkups under Medicare, the Australian public healthcare system.

Getting private health insurance does not mean you give up your Medicare coverage; you can have both at the same time. Under Medicare, you can visit a public hospital as a public patient, but may be placed on a waitlist and cannot select your own doctor.

Medicare also covers your visit to a GP and most of the Medicare Benefits Schedule (MBS) fee for visiting a specialist, so if all you need are basic checkups, you may be fine relying on Medicare alone.

If you do decide to take up private health insurance, remember that you’re entitled to the same cover at the same price as anyone else, regardless of your risk profile. At the same time, if you're going to take out health insurance, it's important to choose a type that you actually use and aren't wasting money on. We go through the different types below.

Hospital cover

Private hospital cover is designed to take the strain off the public health system. To encourage people to join and spread the load across both systems, the government has several financial incentives for people to join a private health insurance fund.

If you’re interested in the financial benefits of private health insurance, or what rebates are available, you can read our article on the tax benefits of private health insurance.

Do I need hospital cover?

With hospital cover, you'll have peace of mind should any medical emergency or illness arise. You could otherwise be out of pocket for thousands of dollars or be put on a long waitlist for surgery.

Here are a few other reasons to take up private hospital cover:

- You get to choose your own doctor in either a private or public hospital.

- If you decide to go to a private hospital, you can choose from any that your provider has an agreement with.

- You have a higher chance of getting a private room when you go to a public hospital as a private patient.

- You may have reduced waiting times for some hospital procedures, such as elective surgery.

- Additional MBS fees and other costs may be covered as part of your policy.

- You can avoid paying the Medicare Levy Surcharge, which applies if you earn over $90,000 per year, or over $180,000 for families.

- You can avoid paying Lifetime Health Cover loading, which applies if you haven't taken hospital cover by the time you're 31.

If you have no problems admitting as a public patient to a public hospital should the need arise, then you may decide you don’t need private hospital cover. If the costs you incur during an unexpected hospital visit are less than the amount you would have spent on hospital cover up until that point, then you could finish out ahead without hospital insurance.

Unfortunately, there’s no way to tell if this will be the case, so many people take out hospital cover just for ‘peace of mind’, especially as they get older and the chances of needing it become more likely.

Here are some reasons to not get private hospital cover:

- Australia's public hospital system is generally good for those needing emergency surgery.

- The premium of your health insurance (which is what you pay for your policy) can be expensive, and unaffordable for many people.

- You may end up in a public hospital anyway for more complex medical conditions or treatments, as public hospitals usually have a wider range of medical equipment.

- You may pay more out of pocket for certain doctors, as private patients are often charged more than public patients, and your health insurance will probably only cover part of the cost.

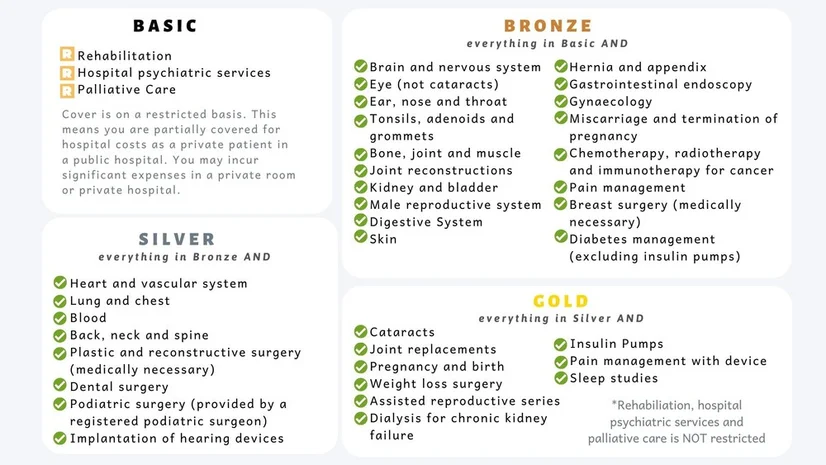

Tiers of hospital cover

The tier system applies only to Hospital Cover and began rolling out in April 2019, becoming mandatory on April 1st 2020. It was designed to make comparison between providers more straightforward by dividing levels of cover into four tiers:

- Basic

- Bronze

- Silver

- Gold

Each of these tiers has its own minimum requirements that must be met in order for a policy to be classified as being part of that tier. These minimum requirements are cumulative, meaning that each increasing tier includes all the minimums of the tiers below it.

This graphic shows the minimal coverage requirements for each tier:

'Plus' policies

There is some wiggle room allowing providers to include additional coverage on top of the minimum requirements for a tier - these are referred to as ‘Plus’ policies. If an insurer offers a policy that provides cover that's above the minimum requirements of a tier, then they can advertise the policy as Basic Plus (+), Bronze Plus (+), or Silver Plus (+). Because a Gold policy covers everything, there’s nothing additional that can be added to it in order to make a ‘Plus’ version.

For example, surgery to remove wisdom teeth is covered under Dental Surgery, which is mandatory for Silver cover, but not Bronze. However, a provider may choose to include it on top of their normal Bronze policy to create a Bronze Plus policy.

This means you can claim this benefit without the full price increase that would come with an upgrade to Silver. This allows you to avoid paying for other mandatory benefits covered under Silver that you might never use, such as podiatric surgery.

It’s important to note that not all ‘Plus’ versions of the same tier are directly comparable, since each provider may choose to include different clinical categories as optional inclusions. For example, Provider A may offer a Bronze Plus package that includes bloodwork, while Provider B offers a Bronze Plus package that includes reconstructive surgery instead - they are both still Bronze Plus policies.

Extras cover

Extras insurance will help cover the cost of ancillary health needs, like dental care, clinical therapies and prescription glasses or contact lenses. If you don't use these services, you may prefer not to purchase Extras Cover as there is no tax benefit to having it.

If you're after just the basics and don't require more expensive treatments like orthodontics, you'll be able to extract the most value out of an entry-level policy. However, don't expect to get 100% back on your bills; most funds offer a 50-60% rebate.

Do I need extras cover?

There’s more value to be had from Extras Cover when you're using your extras regularly, so assessing your present and potential future needs is the best place to start.

Many providers won’t include extras cover for pre-existing conditions, so if you have a family history of a condition like osteoporosis or diabetes, you may need to be covered before these issues arise so that they’re not counted as a pre-existing condition.

Providers approach extras insurance in different ways. Some will give you a lot of flexibility over which services you want to include, while others have strict packages you must choose from.

If you start by writing down a list of your personal must-haves (e.g. complex dental, physiotherapy, and hearing aids) you can then whittle down the list of possible policies to only those that include exactly what you’re looking for.

If you're getting cover for your family or if you're aged between 55 to 79, then there are some perks to getting extras insurance:

- Families pay the same premium as couples, so children are covered for free. However, children under 5 on average typically get less than $100 in benefits each year, while children between 10 and $14 typically get almost $400.

- People aged 55 to 79 tend to get more use of extras insurance benefits than other age groups, and typically receive an average benefit of over $600 a year.

Dental cover

One of the most popular reasons to take out extras is dental cover. Dental is typically split into different levels of cover from routine or general up to major and complex procedures, with orthodontics usually being a separate option as well.

Additionally, depending on what procedures you have done and where, not everything may be covered under your Extras policy. For example, if you elect to have wisdom teeth taken out in a hospital, some of the hospital and doctor fees may not be covered under your Extras policy and you’ll have to pay these out-of-pocket.

Combined cover

Combined cover is hospital cover and extras cover combined in a single policy. Private hospital and extras insurance are different types of insurance, and you don't necessarily need both. Often, you can get a better deal by buying extras and hospital cover from two separate health funds.

Some people like the convenience of having to only deal with one health fund for both insurance types. Before you take out combined cover, think about whether you need both hospital and extras insurance.

Ambulance cover

Ambulance cover is the most basic type of cover, and covers the cost of an ambulance in an emergency.

Unless you live in Queensland or Tasmania, ambulance call-out fees are not covered under Medicare and will have to be paid for out-of-pocket. You can find out more about ambulance fees for your state in our ambulance cover article.

When shopping around, check with an insurer to see what kind of ambulance cover they offer. Some only offer ground transport in an emergency and will not offer air ambulance. Some might just cover emergency ambulance and exclude transport to transfer patients between hospitals.

What to consider when choosing health insurance

Once you've decided what level of cover is right for you, you can start comparing different providers and policies. Each policy will have a product disclosure stateent (PDS) - read these to understand the inclusions and exclusions.

Here are some more things to consider when choosing health insurance.

Your personal circumstances

What's going on in your life will usually have a significant impact on which type and level of cover will best suit you.

Consider the following questions:

- Do you have any pre-existing conditions that may require medical treatment in the near future?

- Are there any hereditary health conditions in your family that could have an impact on you?

- Are you planning on starting or growing a family and will you require obstetrics cover?

- Do you need cover for partners or dependants?

- How will your health needs and requirements change as you get older?

You should be honest about your health history when you take out a policy. Your insurer may not pay your claim if they believe that you have misled them.

Premiums

Generally, the higher your premium, the more benefits you can claim. You can usually tweak your health insurance policy to make your premium more affordable. Consider doing the following:

- Customise your excess. Choosing a higher excess (what you agree to pay towards a Hospital claim) will usually reduce your premiums.

- Choose a co-payment. This is a fee that you agree to pay for each day you're a patient in a hospital. It could be a more affordable option if your co-payment is less than what the excess would be and if you know how long you'll need to stay in hospital.

Waiting periods

Most health funds have a waiting period before you're able to claim on any services. The length of the waiting period usually depends on the type and complexity of the medical treatment.

- For hospital cover, waiting periods for pre-existing conditions or obstetrics (pregnancy) are usually 12 months.

- Waiting periods for extras vary; it can be 2 months for many services, and is usually 12 months for major dental treatment.

- Waiting periods typically won't apply if you're switching policies or health funds to a similar level of cover.

Decision time

One thing to remember that will help you avoid confusion when browsing policies is that hospital cover is sorted into Basic / Bronze / Silver / Gold tiers, while extras will be called whatever marketing name the provider has come up with for themselves (e.g. 'Lifestyle Extras,' 'Black Extras 60,' 'Essential Extras,' or 'Top Extras.')

It may be possible to mix-and-match your hospital and extras cover in many ways, such as combining the most expensive hospital cover with the most basic extras cover or vice-versa. Your provider may also offer some pre-selected hospital & extras combinations.

ProductReview.com.au is a great tool for seeing feedback about Health Insurance providers from real customers. You can browse our list of health insurance providers and easily see a summary of how other Australians rate their health fund for customer service, value for money, and transparency.

If you click through to an individual fund, you can use the Filter Reviews button to narrow down the reviews to see just those that are similar to you, or that you might be interested in reading.

Remember: insurance isn't forever. Reassess your policy regularly to ensure that it's meeting your needs and you're making the most of it.

This article is part of our series on private health insurance.

Disclaimer: The information on this website is for general information only. It should not be taken as constituting professional advice from the website owner - ProductReview.com.au. ProductReview.com.au is not a financial adviser. You should consider seeking independent legal, financial, taxation or other advice to check how the website information relates to your unique circumstances. ProductReview.com.au is not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly, by use of this website.

Hi Usman, thanks for reviewing Australian Unity.… Read more