Best Home Loans

Aussie Home Loans 🏆 2026

4.9We’ve helped over 1.5million + customers find the right home loan for them.

Aussie Home Loans 🏆 2026

- See all

Great Prompt efficient service. Recommend to anyone who wants promo easy finance

Lendi 🏆 2026

- See all

Natalie was very helpful, easy to contact and responded quickly to any questions I had.

Mortgage House 🏆 2026

- See all

Mittal’s service has been outstanding the whole time we have worked with him looking for an investment property for our super fund. I would… Read more

recommend using Mortgage House and will use them again. Thank you for all your knowledge and excellent communication Mittal.

Home Loan Experts

- See all

Mohit, Bibesh and Prajita, my family and I can’t thank you enough for all your hard work to get us into our home! From start to finish the team have been absolutely outstanding!!

Mortgage Domayne

- See all

I had a positive experience refinancing my home loan with this company. The customer service was professional, helpful, and responsive throughout the… Read more

process. I am satisfied with the interest rate I received, as it was competitive and suited my needs. Overall, I appreciate the smooth and efficient support provided by the team.

Loan Gallery Finance

- See all

We had an excellent experience working with Darryl Cracknell. He is knowledgeable, responsive, and made the entire process straightforward from start… Read more

to finish. He took the time to explain our options clearly, kept us informed every step of the way, and worked hard to secure a great outcome for us. We highly recommend Darryl to anyone looking for a reliable and trustworthy mortgage broker, whether it is your first home or an investment loan.

Loan Studio

- See all

Great broker Steve Mottau and Joe Adriano have been my loan brokers for 5 years now. I have been getting my property and investment property… Read more

financed and refinanced multiple times. Steve is very proactive, professional, transparent, and highly customer-centric. He spends a lot of time understanding your requirements and providing multiple options for refinancing your loans that benefit you so you can pay lower interest and get the maximum tax benefit. He proactively approaches you if there is a better loan option and cashback provided by some banks, and helps you refinance your loan to get maximum benefit. I have refinanced my loan on my property a couple of times in the last 5 years and have got thousands of dollars in cashback and very good interest rates. Once you have decided on the bank, Joe comes in and helps you get all the documents in order and works with the bank to make the entire process seamless. I had to only review and sign the documents. The rest was handled by Joe. Both of them have been wonderful brokers, and I have recommended them to my friends.

Mortgage Ezy

Highly recommend the products which provide the solutions for us. The customer services are quite good at timely manner with efficiency.

Loan Market

- See all

Stay away at all costs!!! I called a few years ago when I was in personal and financial trouble. I was bluntly told that I had wasted their time, was an idiot, and that my wife destroyed me. Avoid!!! Horrendous!! They will throw you under he bus!!

Future Assist Group of Companies

Future Assist has assisted us to plan for retirement and has reduced the stress and overwhelm of this process immeasurably. We are grateful that we are looking good for retirement when we are ready.

Pepper Money Home Loans

- See all

Pepper are a joy to deal with, application process was professional and efficient

Community First Bank

- See all

I have been with this credit union/ bank since it was Elcom Credit Union so it must be about 40 years , during the early years they looked after me… Read more

when I desperatley needed help but as the years have gone on thankfully I do not need help anymore. I moved to the mid north coast 8+years ago but I still remain a customer and always will. THANKYOU.

Homestar Finance

- See all

Great experience from start to finish. Homestar made the home loan process smooth and stress-free. They made securing our home loan on time. Highly recommend to anyone looking for a home loans.

Reduce Home Loans

We had an outstanding experience working with Kurt and couldn't recommend him more highly. From our initial enquiry through to settlement, Kurt made… Read more

the entire process smooth and stress-free. He was communicative every step of the way, keeping us informed, answering our questions promptly, and always making himself available whenever we needed guidance. Kurt is incredibly knowledgeable, thorough and professional. He took the time to explain every stage of the process, presented us with the best options for our circumstances, and ensured everything progressed as efficiently as possible. His attention to detail and proactive approach gave us complete confidence throughout our property purchase. It was an absolute pleasure working with him, and we would not hesitate to recommend his services to anyone seeking a mortgage broker. If you're looking for someone who is experienced, reliable and genuinely invested in his clients, Kurt is the person to call. Thank you again Kurt, and we look forward to working with you again in the future.

Credit Hub Australia

Great Service provided by Himal Shah and looking forward to work with him for my financial portfolio. We approach Himal for personal loan, and he… Read more

was efficient to provide options and offered us best product with best interest rates. I will recommend family and friends to contact Himal for all finance requirements.

Mortgage Broker Melbourne

Anne and Eddy were both superb. Anne, who I had most contact with, was a godsend: extremely personable, professional and highly efficient. Without… Read more

her (and Eddy's) support I don't know how we would have survived this arduous process of selling and buying houses.

UNO home loans

Our family just had our 4th loan arranged by Uno. Three were not straightforward loans at all being in our superannuation fund (knocked back by… Read more

another broker) and the 4th was for a recent arrival to Australia with no work history here & self employed. Mike Parsons worked miracles. He didn't take no for an answer, thought outside the box and his wisdom, multiple lender options, & sheer hard work & tenancity paid off for us. Nothing was too much trouble. We will be forever grateful! Thanks Mike!!

Professional Partners

Expertise and efficiency that is second to none – Chantal's expertise and her team's efficiency allowed us to choose the best loan product that suited our needs. Best of all, we learned a lot from… Read more

the process, enabling us to make an informed decision and plan for the future. Transparent and very quick turnaround times. The service that Mortgage Domayne provides is second to none. Thanks again, Chantal and your team!

ARG Finance

Our journey with the new home build has been a pleasant experience with the support of Ginny taking care of all our financing needs. I would like to… Read more

thank Ginny for his services in supporting our dream for a new home and for providing me with sound financial advice regarding the new home and previous investment properties. I recommend anyone who needs financial advice to utilities Ginny and his team who provide excellent information and support whilst doing so with a smile in what can be a stressful time navigating finances. I look forward to utilising Ginny brokering services again in the future.

Greenline Home Loans

Joseph Dabas is simply the best in the industry.... Greenline should give him a pay rise. Two years ago we purchased our first home - Joseph made… Read more

that dream come true. Recently we remortgaged with Joseph & he got us the best interest rate going. His industry contacts & networking set him aside from many other brokers. His care factor for doing the right thing by his customer is second. Our family has put trust in him twice now & he has delivered. I now recommend anyone looking for finance to contact Joseph.

Athena Home Loans

- See all

When my wife and I upgraded to a new home a few years back, we went straight with Athena instead of going back to our Big 4 lender from our first… Read more

home loan. Five years on, we're still with them on a Power Up owner-occupier variable loan with offset, and the decision has held up well.

The rate was noticeably lower at signup than what our old lender quoted us, and what's kept us with Athena is their same-rate policy. Existing customers pay the same rate as new customers on the same product. It means we don't have the "loyalty tax" problem, where you have to threaten to refinance every couple of years just to get the rate you should already be on. Rate changes also get passed on quickly after RBA decisions, which was a welcome change.

Settlement was fast and simple. The app is clean and does what we need. One thing worth knowing before you switch: Athena has no branches at all. Customer service is available by phone, email and chat. That works fine for us, but if you're someone who prefers walking into a branch to sit down with a banker in person, it's a real trade-off to weigh up.

Happy enough with Athena that I share my personal referral code publicly online (see the disclosure on this review).

Mel Finance Services

First time buyer. Lumbini was informative and took the time and care to understand our needs. Was super helpful in providing an analysis against… Read more

different lenders so we could make an informed decision. Very knowledgeable and responsive. Thanks Lumbini! Daniel

Well Money

For using Bendigo Bank 1 star! Why partner with the worst bank in Australia?

Resimac

- See all

⭐⭐⭐⭐⭐ I had an excellent experience with Resimac throughout my home loan journey. The application and settlement process was smooth, and the team… Read more

was professional, responsive, and supportive at every stage. They communicated clearly, answered all my questions promptly, and worked efficiently to achieve a successful outcome.

Thank you for the outstanding service!

MyChoice Home Loans

- See all

I had a great experience with Adam. He kept me in the loop and made it a nice and smooth process. Thank you!

Tiimely Home

- See all

Timely Home customer since 2022, I was very satisfied with them until Timely migrated backend from Adelaide Bank to Bendigo Bank in December 2025,… Read more

and introduced their new total nightmare Timely app. Since migration, I have faced serious issues in accessing statements and reports on my balances. Home loan balance statements are now generated once a 6 month - that also you have to beg support on chat. Offset statements never generated on time, again beg to support on chat. There was no prior communication around change of statements and frequency. I will not recommend Timely to anyone because they lack reliability and service for a Home loan operator. I raised this issue in a tribunal - in response all they did was finger pointing and blaming Bendigo for their inability to generate statements.

Unloan

- See all

Unloans advertised rate today 5.89 vs my rate "the interest rate which will apply to your loan is 5.96%" with a 3yr discount of 0.03%. I started off… Read more

with the advised rate but over time I didn't receive the same changes as the advised rate. So at this rate with the "Loyalty Bonus" of 0.01% off per year I might match your advertised "New Customer" rate in another 7 years a total of 10 years just to match with a new customer at day one!!! Not much of a difference but it sure is irritating. Please don't reply saying funding costs blah blah blah...... Why is it that funding costs are never in the customers favour???

What If We Finance

Some people are exceptionally good at what they do. Others leave a lasting impression because of the way they make people feel. Spiro does both. From… Read more

our very first conversation, we knew we were in capable hands. Spiro combined remarkable industry and technical expertise with genuine warmth, making what could have been an overwhelming process feel calm, manageable and even enjoyable. He was always approachable, responsive and generous with his time. No question (and I had many!) was ever too much. Every conversation was met with patience, honesty and clarity. Spiro communication was exceptional. He kept us informed every step of the way. He always followed through on what he said he would do. His calm confidence, good humour and unwavering professionalism gave us complete trust throughout the entire journey. He took the time to understand our circumstances, saw the bigger picture, and worked tirelessly to achieve the best possible outcome for us.

Investors Mortgage

Aarjoo helped me alot with all the process. She was so patient with everything. Very quick at replying and sorting documents. Would 100% recommened her for anyone else need help with their loan or mortgage.

Refinancer

I have been honoured to be a client of this company for years now and frequently utilise their expertise and services. Hayden and his team are always… Read more

very helpful with financial advice and making changes that are advantageous to me. They recently helped me refinance my mortgage to a better rate and saved me a lot of money. The process was quick and efficient and all my questions were answered the same day. They go to great lengths to make sure i understand all the details and always get a very good outcome. They have never let me down. I would highly recommend this company to anyone needing financial advice. Kim rida

Aussie Home Loans 🏆 2026

4.9We’ve helped over 1.5million + customers find the right home loan for them.

Types of loan providers

Banks

The Big Four banks - that is, Commonwealth Bank, NAB, Westpac, and ANZ - dominate the home loan market. There are also plenty of smaller, more local banks (think banks like Bendigo Bank and ING) that offer a variety of home loans - so do some international banks that operate in Australia.

Non-bank lenders

Non-bank lenders are those which don’t hold a banking license - they’re not a bank, a building society, or a credit union. These lenders still have to follow the same laws, rules and regulations as banks, so they’re still as safe to use as traditional banks.

Online lenders - such as Lendi, Athena Home Loans, and Tic:Toc Home Loans - fall into this category, and are on the rise thanks to the convenience and competitive rates they offer.

Is it worth getting a mortgage broker?

If you’re having difficulty comparing loans and lenders, then a mortgage broker may be able to help you find the right loan for you. This is a licensed professional who brings borrowers and lenders together, and helps you apply for the loan and assist you throughout the process through to settlement.

Often home loan brokers are paid commission by lenders, so you don’t have to pay for their services. They may however be offered incentives by a lender to offer you certain loans, which could influence which loans they recommend to you.

What to consider when you compare home loans

Eligibility

Different lenders have different eligibility criteria for taking out a home loan, so ensure that you check the requirements of each lender you’re considering so that you don’t waste your time with a lengthy application process.

Depending on your situation, you may also be eligible for a government incentive, such as the First Home Owner Grant - this grant requires that you move into your new home within 12 months, and live in it for at least 6 months.

Loan purpose

You should ensure that the type of loan you’re taking out is the right option for your loan purpose, depending on whether you’re a first-time home buyer, refinancing your mortgage, buying an investment property, looking for a construction loan, or something else.

A construction loan, for example, differs from a regular home loan in that it progressively lets you access money as you complete different phases of your home’s construction.

Loan repayment type

There are 2 ways to repay your loan: with principle and interest repayments, or with interest-only repayments.

Principal and interest repayments

Most Australians get this type of loan. With this loan, you make regular repayments on the principal (the amount borrowed), and you pay interest on that amount. These generally have a lower interest rate than interest-only loans, and you’ll usually own your home sooner.

Interest-only repayments

For interest-only home loans, you only make repayments on the interest on the amount borrowed for an initial period of time. Because you’re not making repayments on the principal, your debt doesn’t reduce.

While your mortgage repayments might be lower during the interest-only period, they’ll increase after that, so you have to ensure that you can afford this.

Initial deposit amount

When you take out a loan, you’ll have to make a home loan deposit, which is usually at least 10 to 20% of the purchase price.

While most lenders require a deposit of 20%, some will allow low deposit home loans, but you’ll likely have to pay Lender’s Mortgage Insurance (LMI) - this protects the lender against any losses in the event that you’re unable to repay your loan.

However, first home buyers may be able to buy a property with as little as a 5% deposit home loan without forking out for LMI under the Australian Government’s First Home Loan Deposit Scheme.

A higher deposit means you borrow less (as you have a lower loan amount) and pay less interest over the life of the loan. You might also be able to score better home loan interest rate deals that can mean even more savings in your pocket.

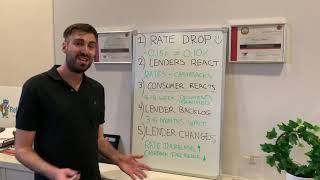

Interest rate and type

It’s recommended to aim for the lowest possible interest rate on your loan, as even small differences between these mortgage rates can wind up saving you thousands over the loan.

When taking out a home loan, you can choose between a fixed rate or a variable rate.

Fixed home loan rates

Fixed rate home loans have an interest rate that stays the same for a set period of time (for example, 5 years). The interest rate then turns into a variable rate.

Variable home loan rates

A variable interest rate in a housing loan can fluctuate depending on changes in the market.

If you’re not leaning towards either of these, you can also get a partially-fixed rate, or a split loan. This means that part of your loan (you can decide how to split it) has a fixed rate and the remainder has a variable rate.

Budget better by knowing your monthly repayment

Your monthly repayment is a figure that represents how much you have to pay each month on a loan. This helps you know exactly what you’re signing up for, so you’re not stretched too thin, or conversely, not paying less than what you can afford.

If it suits you better, you can also calculate your weekly or fortnightly repayment.

Loan features

Some loans have extra features that can give you greater flexibility in how you access and use them. However, these features usually come at a higher cost, so you should weigh up your options to see if you’ll use them in a way that makes the higher price worth it.

- Offset account: This is a transaction account that’s linked to your home loan. The balance of this account can be offset against what you owe on your home loan.

- Extra repayments: A loan that lets you make extra repayments lets you pay off your loan faster, saving you in paying interest. Most variable rate loans allow this, while some fixed rate loans limit how much extra you can repay.

- Redraw facility: This lets you withdraw any extra payments you’ve made on your loan, which can be useful for emergencies. Your lender may charge a redraw fee or restrict how much money you can redraw.

- Portability: With a portable home loan, you can sell your home and purchase a new one with the same home loan, without needing to refinance.

- Line of credit: A line of credit home loan lets you borrow some of the built-up equity in your home. You can withdraw up to a certain amount (the credit limit) determined by your lender.

Loan term

The loan term refers to the length of time you have to pay off your loan. A typical loan term is 30 years, although depending on your situation, you can also find terms ranging from around 20 to 40 years.

It’s generally recommended to get the shortest loan term that you can afford - you’ll have to make higher home loan repayments, but you’ll pay less interest, saving you more in the long run.

Fees

You should read the fine print to figure out all the fees associated with your home loan, so you’re not surprised with a large sum down the track. Usually you’ll have to pay an application fee (also called an establishment, up-front, or set-up fee), which is a one-off payment that you pay when starting your loan.

You’ll probably also have to pay ongoing fees, such as service fees that are charged periodically (usually monthly or yearly) to a lender for administering your loan.

Find the comparison rate to know exactly what you’re paying

The comparison rate of a loan is the sum that indicates the cost of the loan, including the interest rate and most fees. This includes all upfront and ongoing costs, so you’ll get a good idea of how much you’ll be forking out over your loan.

If you’re tossing up between a few different loans, this figure can help make choosing between your options easier.

Comparing loan providers

When comparing providers, you should also look into the following:

- The application process. The application process should be relatively simple, and should suit your needs. For example, if you need to organise a loan quickly, then you may want to opt for an online lender who can offer faster results.

- The transparency of the lender. A lender should be upfront with you with all information relating to your loan, whether it’s positive or negative.

- The lender’s customer service. Your home loan doesn’t end after you’ve finished your application, which is why timely, helpful customer service is important to make things as easy as they possibly can be for you.

Reading online reviews can help you determine the overall experience and quality of care a lender can give you, as well give you an indication of how straightforward the application process is.

The bottom line

You should be realistic about how much you can borrow. Take into account rising interest rates that could mean increased loan repayments for you - giving yourself a bit of breathing room, and considering how your personal and financial circumstances could change should help you find a loan that’s right for you.

Disclaimer: The information on this website is for general information only. It should not be taken as constituting professional advice from the website owner - ProductReview.com.au. ProductReview.com.au is not a financial adviser. You should consider seeking independent legal, financial, taxation or other advice to check how the website information relates to your unique circumstances. ProductReview.com.au is not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly, by use of this website.

Hi Tommy, we appreciate your feedback. If you would like,… Read more